Small business owners strive to offer attractive benefits packages to retain talented employees, with nearly half considering leaving due to inadequate benefits. Among the essential benefits are Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs), offering tax-free savings for healthcare expenses. However, understanding the differences between these accounts is crucial for optimizing benefits strategies and reducing tax burdens.

HSA (Health Savings Accounts)

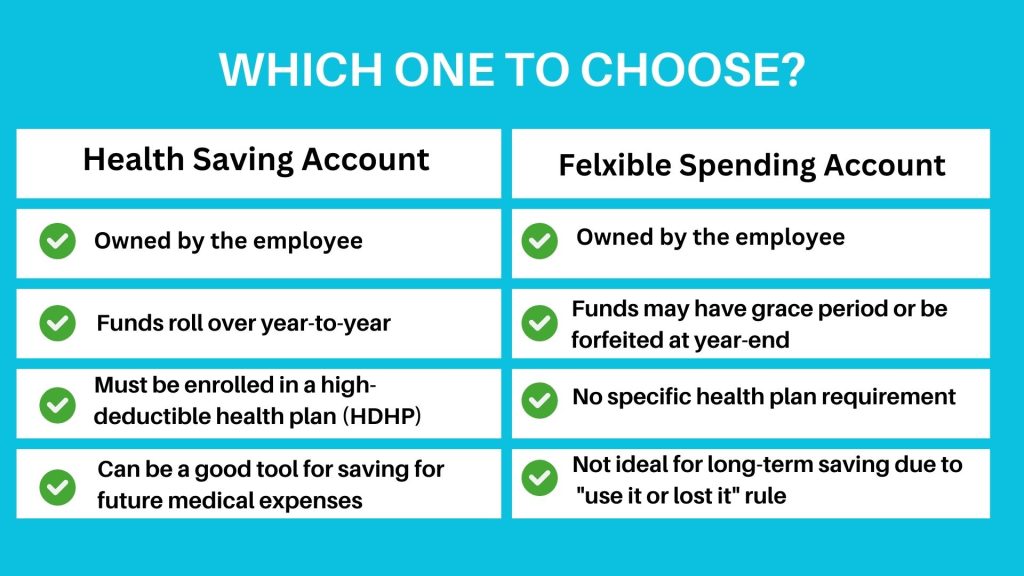

An HSA is a special savings account for people with high-deductible health insurance (HDHP). It lets you save money before taxes for medical expenses like deductibles, prescriptions, or dental work. The money rolls over each year, so you can save up for future medical costs. This can be a good way to lower your overall healthcare costs if you have an HDHP.

Why Should You Choose an HSA?

There’s something called a triple-tax advantage.

Contributions are tax-deductible.

Earnings on investments within the HSA grow tax-free.

Withdrawals for qualified medical expenses are tax-free.

Let’s say you put $1,000 into a Health Savings Account. This $1,000 reduces how much you pay taxes on. That’s the first advantage. If you pick a good HSA provider, you can invest that

$1,000 in stocks or bonds, and it can grow. The money you make from these investments doesn’t get taxed. That’s the second advantage. Plus, when you take money out of your HSA later to pay for medical stuff, you don’t have to pay taxes on the money you make.

Benefits for Employers:

Cost Savings: HSAs are often paired with high-deductible health plans (HDHPs), which have lower premiums for the company. Even with contributions to employee HSAs, the overall cost can be lower.

Tax Advantages: Employer contributions to employee HSAs are tax-deductible as a business expense. Additionally, payroll taxes aren’t applied to these contributions.

Attracting and Retaining Employees: HSAs can be a valuable benefit, making your company more competitive in attracting and keeping talent.

Benefits for Employees:

Tax-Free Savings: Contributions to HSAs are made with pre-tax dollars, reducing taxable income.

Long-Term Savings: Unused funds in the HSA roll over each year and can be invested for tax- free growth, similar to a retirement account.

Portability: Unlike some health savings plans, HSAs are owned by the employee. They can keep the account and any funds even if they change jobs.

Tax-Free Withdrawals: Money used for qualified medical expenses is tax-free. This includes deductibles, co-pays, and prescriptions.

IRS Updates:

The IRS sets contribution limits for HSAs each year. For 2024, the limits are:

Individual coverage: $4,150

Family coverage: $8,300

Catch-up contributions for those over 55: $1,000

FSA (Flexible Spending Account )

Flexible Spending Account is an employer-based benefit that lets you set aside pre-tax money to cover health and dependent care costs. This means you pay less in taxes upfront, and can then use the funds for things like copays, prescriptions, or even dependent care. It’s a great way to save on predictable healthcare or dependent care expenses, but be aware that unused funds typically don’t roll over to the next year. FSAs are offered by employers and you can only contribute to an FSA if your employer offers it as part of their benefits package.

There are two types of FSAs:

Healthcare FSA: Used for medical expenses.

Dependent Care FSA: Used for dependent care costs like childcare.

Why Should You Choose an FSA?

Benefits of FSAs for Employers

Reduced Payroll Taxes: Employers save on payroll taxes (Social Security and Medicare) on the amount employees contribute to FSAs.

Attractive Benefit Option: Offering FSAs can help attract and retain employees, especially those with predictable healthcare expenses.

Easy to Set Up: FSAs can be established with most existing health insurance plans.

Benefits of FSAs for Employees

Tax Savings: Employees save money on taxes by contributing pre-tax dollars to cover qualified medical and dependent care expenses.

Budgeting Tool: FSAs help employees plan and manage their healthcare expenses throughout the year.

Upfront Access to Funds: Employees can access the full amount of their contribution at the beginning of the year, even if they haven’t paid it in yet (pre-funded).

Wider Range of Qualified Expenses: FSAs now cover over-the-counter medications and menstrual products, expanding what you can use the funds for.

IRS Updates:

The IRS sets contribution limits for FSAs each year. For 2024, the limits are:

FSA contribution limit for 2024: $3,200

Spouses with separate FSAs can contribute up to a combined total of $6,400

Employer contributions are possible (not included in employee limit)

What Should a Small Business Consider?

HSAs offer more long-term savings potential for healthy employees, while FSAs provide a simpler way to save on predictable medical expenses. HSAs are generally considered better due to the triple tax advantage and potential for long-term savings with investments. FSAs can be a good option if you’re not HSA-eligible or have predictable medical expenses throughout the year.

Tax Benefits for Small Business Owners:

Employer contributions to these accounts are tax-deductible as a business expense, lowering your taxable income. Additionally, employee contributions are made with pre-tax dollars, reducing payroll taxes for both you and your employees.

HSAs Offer an Additional Tax Advantage:

Unlike FSAs, any earnings or interest generated on the funds in an HSA grow tax-free. This can be a significant benefit for long-term savings.

But, you cannot contribute to both an HSA and a healthcare FSA in the same year. However, you can contribute to an HSA and a dependent care FSA in the same year. Also, you can’t change your FSA contribution amount in the middle of the year unless you experience a qualifying event such as marriage, birth of a child, or job loss

Bottom Line:

While both HSAs and FSAs offer tax advantages for small business owners, HSAs provide a slight edge due to the potential for tax-free growth on account earnings. However, the best choice ultimately depends on your employee demographics and what would be most beneficial for them.

Still unsure whether an HSA or FSA is the right fit for your small business? Don’t worry! At Taxfully, we understand the unique needs of each business. Schedule a FREE consultationwith our tax specialists today to discuss your specific situation and explore the best option for maximizing your tax savings.