✅ SEP-IRA: simplified employee pension plans are easy to set up and involve minimal paperwork. Employers make all contributions, up to 25% of an employee’s income or $69,000 in 2024. These plans are ideal for businesses with few employees due to their high contribution limits and flexibility.

✅ SIMPLE IRA: savings incentive match plan for employees allows both employer and employee contributions. The employee contribution limit for 2024 is $16,000, with an additional

$3,500 for those 50 or older. Employers must match employee contributions up to 3% of compensation or make a 2% non-elective contribution.

✅ Traditional 401(k): allows employees to contribute a portion of their salary with tax-deferred earnings. The contribution limit for 2024 is $23,000, with an additional $7,500 for those 50 or older. Employers can also contribute, offering significant tax advantages.

✅ SIMPLE 401(k): similar to SIMPLE IRAs but with an additional option for employees to take loans against their accounts. Contributions are limited to $16,000, with catch-up contributions allowed for those 50 or older.

✅ Solo 401(k): designed for self-employed individuals, allowing contributions as both employer and employee. Contribution limits for 2024 are $23,000 for employee deferrals, plus employer contributions up to 25% of compensation, with a total cap of $69,000. If your business has no employees other than your spouse, a Solo 401(k) is ideal.

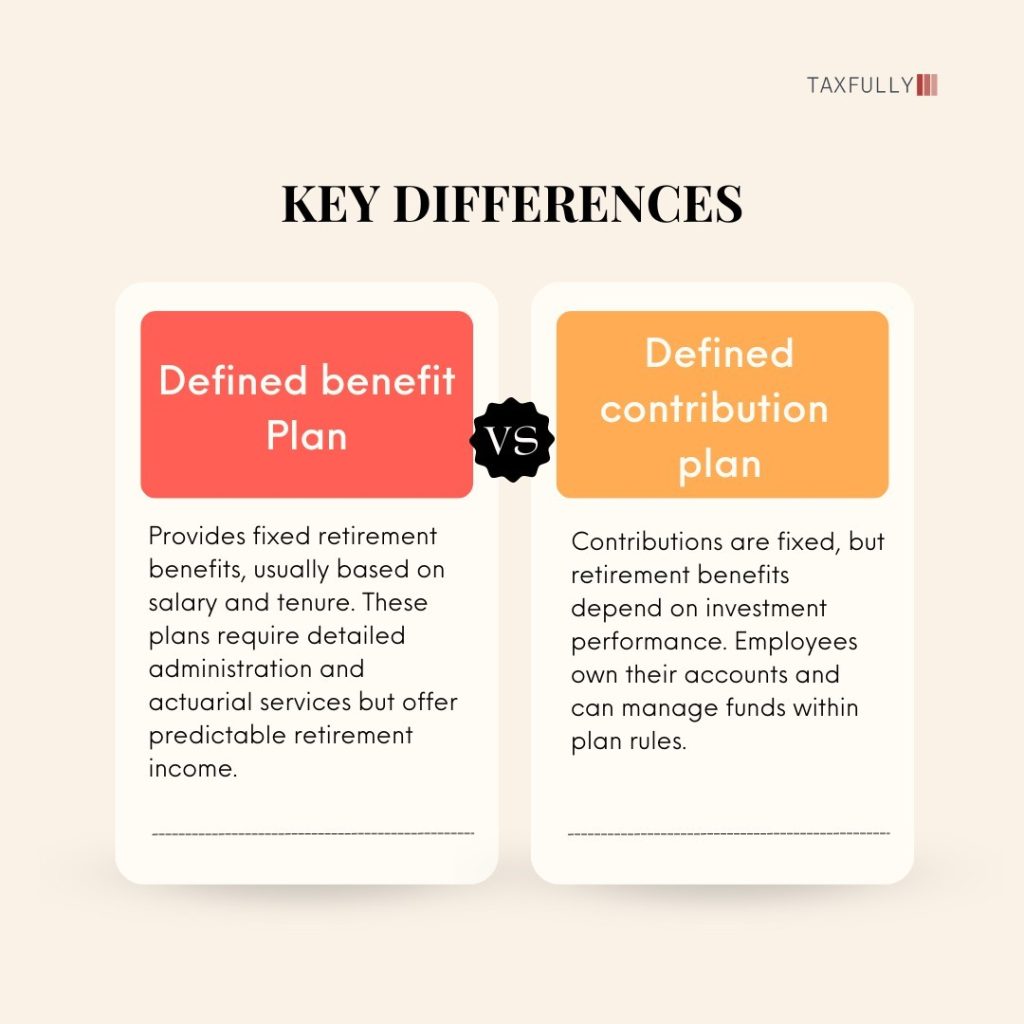

✅ Defined Benefit Plans: these plans provide a specified retirement benefit, usually based on salary and years of service. They are less common today but can offer generous benefits for high-income professionals who can manage administrative costs.